Financing a new car versus a used car is defined by one core trade-off: lower interest rates on new vehicles versus lower purchase prices on used ones. The average new car loan rate sits around 6.37% APR compared to 11.26% APR for used cars. That nearly 5 percentage point gap translates to roughly $3,900 more in interest over a 60-month loan on a comparable used vehicle. For Australian buyers weighing up new vs used vehicle finance in 2026, the right choice depends on your credit score, how long you plan to keep the car, and how well you understand the total cost of ownership beyond the sticker price.

How do interest rates and credit scores affect financing a new vs used car?

Lenders price new car loans lower because new vehicles carry less risk. A new car has a known value, a factory warranty, and no hidden mechanical history. Used cars are harder to value accurately, which means lenders charge more to cover that uncertainty.

Your credit score changes the picture dramatically. Excellent credit borrowers with scores of 781 or above qualify for new car loans at around 4.88% APR. Subprime borrowers face rates as high as 19% on used vehicles. That gap between the best and worst rates is far wider than the gap between new and used car rates at the same credit tier.

The factors that shape your rate include:

- Credit score tier: The single biggest lever on your rate. Moving from fair to good credit can save more than aggressive price negotiation.

- Loan term length: Shorter loan terms carry rates 0.5–1 percentage point lower than 60-month loans. An 84-month loan on an older used car is the highest-risk combination.

- Vehicle age: Lenders often restrict loan terms on older vehicles. A car more than 10 years old may only qualify for a 36 or 48-month term.

- Lender type: Credit unions typically offer lower rates than dealership finance offices. Online lenders add competitive pressure that benefits borrowers who shop around.

Pro Tip: If your credit score sits just below a tier cutoff, focused credit repair over 60–90 days can unlock a meaningfully better rate. That improvement often delivers more savings than any amount of dealer price negotiation.

Understanding what affects your car loan rate before you apply puts you in a far stronger position at the dealership.

What are the upfront and ongoing cost differences when buying a new car vs a used car?

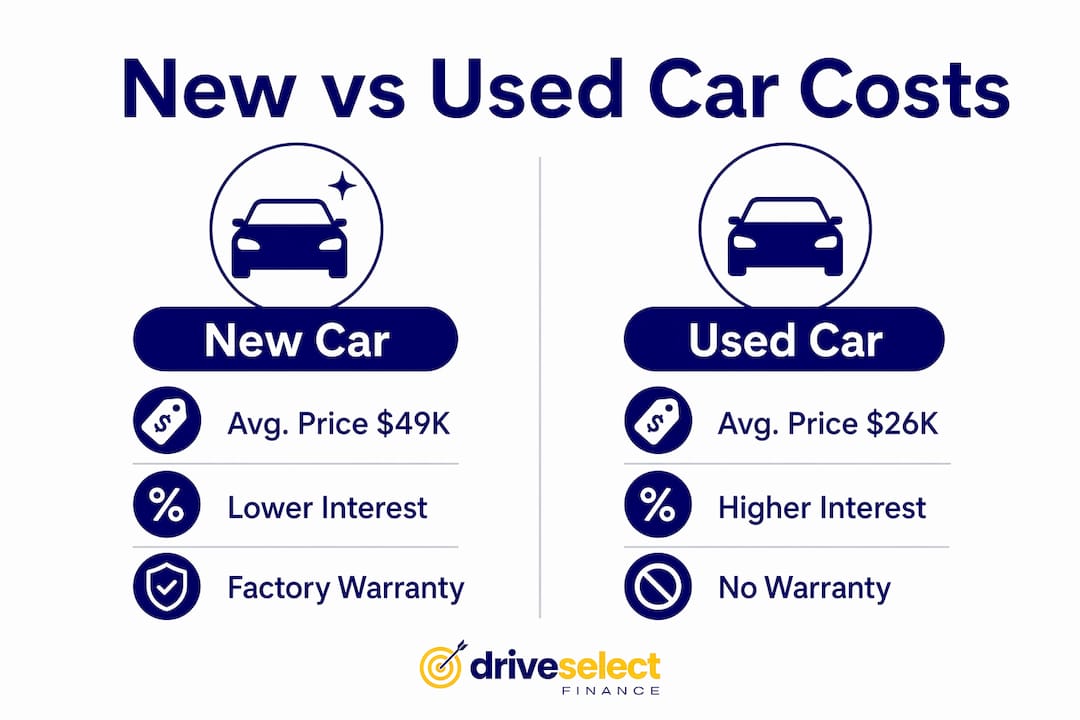

The purchase price gap between new and used cars is substantial. New vehicles averaged $49,191 in recent market data, while used cars averaged between $25,500 and $26,000. That $23,000+ difference looks like a clear win for used cars until you factor in depreciation, maintenance, and insurance.

New cars lose 20–30% of their value within the first 2–3 years. That depreciation hits hardest in the early months of ownership. A buyer who finances a new car and sells it after two years absorbs that loss directly. A buyer who purchases a two-year-old used car lets the first owner absorb it instead.

| Cost Factor | New Car | Used Car |

|---|---|---|

| Average purchase price | ~$49,191 | ~$25,500–$26,000 |

| Depreciation risk | High in first 2–3 years | Already absorbed by prior owner |

| Warranty coverage | Full factory warranty | Limited or none |

| Maintenance costs | Low in early years | Higher, less predictable |

| Insurance premiums | Higher (higher value) | Lower (lower value) |

New cars come with comprehensive factory warranties that cap repair costs during early ownership. Used cars carry no such protection unless a dealer warranty or extended cover is purchased separately. Maintenance costs on a used vehicle can offset the savings on purchase price faster than most buyers expect.

Insurance premiums follow the vehicle's value. A new car costs more to insure because it costs more to replace. Over a five-year loan, that annual premium difference adds up to a meaningful figure in the total cost of ownership calculation.

How to compare new and used car finance offers to find the best deal

Getting the lowest rate requires comparing multiple lenders before you set foot in a dealership. Comparing loan offers from credit unions, banks, and online lenders can save 1–3 percentage points in interest. On a $25,000 used car loan over 60 months, that equals $700–$2,150 in total savings.

Follow these steps to compare finance offers effectively:

- Check your credit score first. Know your tier before you apply. Errors on your credit file are common and correctable before you seek finance.

- Get pre-approved before visiting a dealer. Pre-approved financing gives you a rate benchmark and removes the dealer's ability to use financing as a negotiation lever.

- Focus on the out-the-door price. Dealers often shift attention to monthly payments rather than total cost. Always negotiate the full vehicle price first, then discuss financing separately.

- Identify add-ons and refuse unnecessary ones. Dealer financing offices frequently bundle paint protection, extended warranties, and gap insurance into the loan principal. Each add-on increases the amount you pay interest on.

- Compare total interest paid, not just monthly payments. A lower monthly payment on a longer loan often means paying thousands more over the life of the loan.

Pro Tip: When buying from a private seller, dealer financing is not available. A pre-approved car loan from an independent lender or broker means you can move quickly and negotiate as a cash buyer.

Driveselectfinance works with a panel of 30+ lenders, which means Australian buyers get genuine rate competition rather than a single take-it-or-leave-it offer.

What financing scenarios make buying new or used cars financially smarter?

The right choice depends on how long you plan to own the vehicle and what your credit profile looks like today.

When new car financing makes more sense:

Buying new is the stronger financial decision when you plan to keep the vehicle for 7–10 years or more. Long-term ownership amortizes the steep early depreciation over a longer period, reducing its impact on your per-year cost. A car that loses $12,000 in value over two years looks very different when spread across a decade of ownership.

Manufacturer incentives including 0% or low-APR financing offers can make new cars genuinely cheaper to finance than used alternatives. When a manufacturer offers 1.9% APR on a new model, the used version of the same car financed at 10% or above may cost more in total interest despite the lower sticker price.

When used car financing makes more sense:

Used cars make financial sense when there is a clear price advantage and you can minimize the loan term or avoid financing altogether. A buyer who puts down a large deposit on a $26,000 used car and repays it over 36 months pays far less total interest than one who stretches a new car loan to 84 months.

Longer loan terms are a genuine risk. 84-month loans on older vehicles create negative equity situations where the car depreciates faster than the loan balance falls. If you need to sell or the car is written off, you owe more than the vehicle is worth. Keeping loan terms at 48–60 months on used cars and 60 months maximum on new cars limits that exposure.

For buyers with credit challenges, a used car with a shorter loan term can be a practical way to build a repayment history before upgrading. Driveselectfinance helps buyers with varied credit profiles find car loan options that match their situation rather than forcing them into unfavorable terms.

Key Takeaways

Choosing between new and used car finance requires comparing interest rates, depreciation, credit score impact, and total loan cost rather than focusing on purchase price alone.

| Point | Details |

|---|---|

| Interest rate gap is significant | New car loans average 6.37% APR vs 11.26% for used, costing thousands more over a 60-month term. |

| Credit score drives your rate | Excellent credit unlocks 4.88% APR on new cars; subprime borrowers face up to 19% on used vehicles. |

| Depreciation favors long-term new car ownership | Keeping a new car 7–10 years spreads early depreciation loss and reduces its per-year cost impact. |

| Pre-approval protects your negotiation | Securing finance before visiting a dealer removes the dealer's ability to use loan terms as leverage. |

| Loan term length affects total cost | Shorter terms carry lower rates and reduce the risk of owing more than the car is worth. |

What I've learned about new vs used car finance after years in the Australian market

The debate between new and used car financing rarely comes down to a single number. Most buyers fixate on the purchase price and miss the bigger picture entirely.

The most common mistake I see is buyers choosing a 7-year loan on a used car to get a low monthly payment. They feel like they are saving money every month, but they end up paying more in total interest than they would have on a new car with a manufacturer's low-rate offer. The monthly payment is not the loan. The total repayment is.

Credit management is underrated in this conversation. A buyer who spends 90 days improving their credit score before applying can shift from a subprime rate to a near-prime rate. That single move saves more money than months of price negotiation at the dealership. Australian buyers often do not realize how much control they have over their rate before they apply.

My honest view is that used cars are the better financial choice for most buyers, but only when the loan term is kept short and the vehicle is genuinely well-priced. A $26,000 used car on a 36-month loan at a competitive rate beats almost every alternative. A $26,000 used car on an 84-month loan at a high rate is one of the worst financial decisions you can make.

Get pre-approved. Know your credit score. Compare at least three lenders. And treat the monthly payment as the last number you look at, not the first.

— Matt

How Driveselectfinance helps Australian buyers get the right car loan

Finding the right car loan means comparing real rates across multiple lenders, not accepting the first offer a dealer puts in front of you.

Driveselectfinance gives Australian buyers access to a panel of 30+ trusted lenders, covering new car loans, used car loans, and everything in between. Whether you are financing your first vehicle or upgrading after years of ownership, the team works to match your credit profile and budget to the most competitive rate available. Explore car loan options tailored to your situation, or speak with a broker who can walk you through the numbers before you commit to anything.

FAQ

What is the interest rate difference between new and used car loans?

New car loans average around 6.37% APR compared to 11.26% APR for used car loans. That gap costs borrowers roughly $3,900 more in interest over a standard 60-month loan term.

Is it cheaper to finance a new or used car in Australia?

Used cars have lower purchase prices, but higher interest rates and maintenance costs can close that gap quickly. New cars with manufacturer low-APR offers can be cheaper to finance in total when you plan to keep the vehicle long-term.

How does my credit score affect my car loan rate?

Your credit score is the single biggest factor in your loan rate. Excellent credit borrowers qualify for new car loans near 4.88% APR, while subprime borrowers face rates up to 19% on used vehicles.

Should I get pre-approved before buying a car?

Pre-approval gives you a confirmed rate before you negotiate, which prevents dealers from using financing as a pressure tool. It also speeds up the purchase process and helps you set a firm budget.

What loan term should I choose for a used car?

Keep used car loan terms at 48–60 months where possible. Longer terms like 84 months increase total interest paid and raise the risk of owing more than the car is worth if it depreciates faster than you repay the principal.