A car budget planning checklist is defined as a structured breakdown of every upfront and ongoing vehicle cost you must account for before committing to a purchase. Most Australian buyers focus on the sticker price and miss the bigger picture. Annual ownership costs average $11,577 per year, or roughly $965 per month, once you factor in fuel, insurance, maintenance, and depreciation. That figure changes how you should think about affordability. The real question is never "Can I afford this car?" It is "Can I afford to own this car for the next three to five years?"

1. What goes on a car budget planning checklist?

Every automobile financial checklist starts with two categories: upfront costs and ongoing costs. Most buyers only budget for the first one.

Upfront costs include the purchase price, stamp duty, registration, and compulsory third party (CTP) insurance. On-road fees typically add $2,000 to $3,000 on top of the advertised price. That gap between the sticker price and what you actually pay at the dealership catches a lot of first-time buyers off guard.

Ongoing costs are where the real money goes. Your monthly car budget must include fuel, servicing, tires, insurance, registration renewals, and depreciation. Depreciation alone averages $4,334 per year for a mid-size vehicle. That is money you lose whether you drive the car or not.

Pro Tip: Write out every cost category before you set a purchase price limit. Buyers who start with the car and work backward almost always underestimate what ownership actually costs.

Here is a quick reference for the major cost buckets:

| Cost Category | Estimated Annual Cost (AUD) |

|---|---|

| Depreciation | ~$4,334 |

| Fuel | ~$2,000–$3,500 |

| Insurance (comprehensive) | ~$900–$1,800 |

| Servicing and maintenance | ~$500–$2,000 |

| Registration and CTP | ~$430–$1,200+ |

The Total Cost of Ownership (TCO) model is the industry standard for calculating what a vehicle truly costs. TCO adds depreciation, interest, fuel, servicing, insurance, registration, and repairs into a single annual figure. Focusing on TCO instead of the purchase price gives you a far more accurate picture of affordability.

2. How to estimate your monthly and annual car expenses

Realistic vehicle cost estimation starts with your loan payment and builds outward from there. Too many buyers calculate the loan repayment, decide it fits their budget, and stop there.

Start with these steps:

- Calculate your loan repayment. Use a loan repayment calculator to model different loan amounts, terms, and interest rates. A longer loan term lowers monthly payments but increases total interest paid.

- Add insurance. Comprehensive cover for a mid-size vehicle runs $900 to $1,800 annually depending on your age, postcode, and claims history. Divide by 12 and add it to your monthly figure.

- Add registration and CTP. These fees vary significantly by state. South Australia charges around $430 per year while the ACT exceeds $1,200. Check your state transport authority's website for exact figures.

- Add fuel costs. Estimate your weekly kilometers, divide by your vehicle's fuel consumption rating, and multiply by the current fuel price. Fuel prices shift, so build in a buffer.

- Add servicing. Toyota and Mazda capped-price servicing averages $250 to $400 per visit. European brands often charge $500 to $1,000 per service. Know your brand before you buy.

- Add an emergency repair fund. Set aside at least $50 per month for unexpected repairs. Servicing complexity has risen with modern vehicle technology, and repair costs are higher than they were five years ago.

Here is what a realistic monthly auto budget breakdown looks like for a mid-size sedan in Australia:

| Expense | Monthly Estimate (AUD) |

|---|---|

| Loan repayment | $350–$500 |

| Insurance | $75–$150 |

| Registration and CTP | $36–$100 |

| Fuel | $150–$280 |

| Servicing (averaged monthly) | $42–$167 |

| Emergency repair fund | $50 |

| Total | $703–$1,247 |

Pro Tip: Industry experts recommend modeling at least three years of total costs before committing to a purchase. A car that fits your budget in year one may not fit in year three when servicing costs climb.

3. What financing steps belong in your car buying financial plan?

Financing decisions shape your monthly budget for the entire loan term. Getting them right before you walk into a dealership is the single most effective thing you can do.

Your car buying financial plan should include these financing steps:

- Check your credit score first. Your credit score directly affects the interest rate you qualify for. A higher rate on a $25,000 loan can cost thousands of dollars more over five years. Understanding what affects your rate before applying puts you in a stronger negotiating position.

- Get pre-approved before you shop. Pre-approval tells you exactly how much you can borrow and at what rate. It also prevents dealerships from steering you toward financing that benefits them more than you.

- Match your loan term to your cash flow. A shorter loan term means higher monthly payments but less total interest. A longer term lowers monthly payments but increases what you pay overall.

- Never borrow to your maximum limit. Running costs add $750 to $900 per month on top of your loan repayment. Borrowing to your ceiling leaves no room for fuel, insurance, or an unexpected repair bill.

- Read the loan contract carefully. Watch for establishment fees, early repayment penalties, and balloon payment structures. These can significantly change the true cost of your loan.

Pro Tip: Treat your pre-approved loan amount as a ceiling, not a target. Buying below your limit gives you a financial buffer that protects you when fuel prices spike or a repair bill arrives.

4. How to track and manage your ongoing car expenses

Car expense tracking is what separates buyers who stay on budget from those who get surprised every quarter. Tracking does not need to be complicated.

Use a spreadsheet or a personal finance app to record every vehicle expense as it happens. Log fuel fill-ups, service invoices, registration payments, and insurance renewals in one place. Reviewing this data monthly shows you exactly where your money goes and where costs are creeping up.

Review your insurance quote every year at renewal time. Loyalty does not always pay with insurance providers. Shopping around annually can save hundreds of dollars on the same level of cover.

Scheduled servicing protects your budget in two ways. First, it prevents small problems from becoming expensive repairs. Second, a complete service history increases your vehicle's resale value. Both outcomes directly affect your total ownership cost.

Pro Tip: Set calendar reminders for registration and insurance renewal dates three weeks in advance. This gives you time to compare quotes and pay on time without scrambling.

Keep a maintenance log in your glove box or a notes app. Record every service, tire rotation, and repair with the date and odometer reading. This record is worth real money when you sell the vehicle.

5. How to adjust your checklist for new versus used vehicles

The financial differences between new and used cars are large enough to change your entire budget approach. Understanding them before you decide is the most useful thing you can do.

New cars lose 20–25% of their value in the first year. That depreciation hit is the steepest part of the ownership curve. Buyers who purchase new absorb that loss immediately. Buyers who purchase a one or two year old vehicle let the first owner absorb it instead.

Certified pre-owned vehicles offer a middle path. They avoid the steepest first-year depreciation while still coming with manufacturer-backed warranties and inspection reports. For budget-conscious buyers, this category often delivers the best value per dollar.

Used vehicles typically cost less upfront and depreciate more slowly. The trade-off is higher potential maintenance costs, especially for vehicles outside their warranty period. A pre-purchase inspection by an independent mechanic costs around $150 to $300 and can save you from buying someone else's problem.

Here is a side-by-side comparison of key budget factors:

| Budget Factor | New Vehicle | Used Vehicle |

|---|---|---|

| Purchase price | Higher | Lower |

| First-year depreciation | 20–25% of value | Much lower |

| Warranty coverage | Full manufacturer warranty | Limited or none |

| Servicing costs | Predictable, often capped | Variable, may be higher |

| Finance rates | Often lower | Can be slightly higher |

| Insurance cost | Higher (higher value) | Lower (lower value) |

For a deeper look at how financing differs between new and used vehicles, the new vs. used car finance comparison covers the key trade-offs in detail.

Pro Tip: If you are buying used, budget an additional $1,000 to $2,000 as a repair reserve for the first year. Older vehicles are less predictable, and having that buffer prevents a single repair from derailing your finances.

Key Takeaways

A complete car budget planning checklist must account for Total Cost of Ownership, not just the purchase price, because running costs average $965 per month across Australian drivers.

| Point | Details |

|---|---|

| TCO over sticker price | Model depreciation, fuel, insurance, and servicing before setting a purchase limit. |

| On-road costs add up fast | Budget an extra $2,000–$3,000 beyond the advertised price for registration, CTP, and stamp duty. |

| Depreciation is the biggest cost | Average depreciation of $4,334 per year makes vehicle choice a major financial decision. |

| Pre-approval protects your budget | Getting pre-approved before shopping prevents overborrowing and dealership pressure. |

| New vs. used changes the math | Certified pre-owned vehicles avoid first-year depreciation while retaining warranty protection. |

What I have learned from watching buyers get this wrong

The most common mistake I see is not buying too much car. It is buying the right car with the wrong budget model. A buyer sets a monthly loan repayment they can afford, signs the contract, and then discovers that fuel, insurance, and the first service add another $800 to their monthly expenses. That gap is where financial stress begins.

The second mistake is treating depreciation as an abstract concept rather than a real cash loss. When you buy a $35,000 car and sell it three years later for $22,000, that $13,000 difference came directly out of your pocket. Buyers who understand this choose vehicles with stronger resale values, like Toyota and Mazda, or buy used to sidestep the steepest part of the depreciation curve.

My strongest advice is to build your budget from the bottom up. Start with your maximum comfortable monthly spend on all vehicle costs combined. Then subtract insurance, fuel, registration, and a servicing allowance. What remains is your actual loan repayment budget. Most buyers do this in reverse and end up stretched.

Regional costs matter more than most buyers realize. Registration and CTP fees differ by hundreds of dollars depending on your state. A buyer in South Australia pays significantly less than a buyer in the ACT for the same vehicle. Factor your state's actual fees into your numbers, not a national average.

— Matt

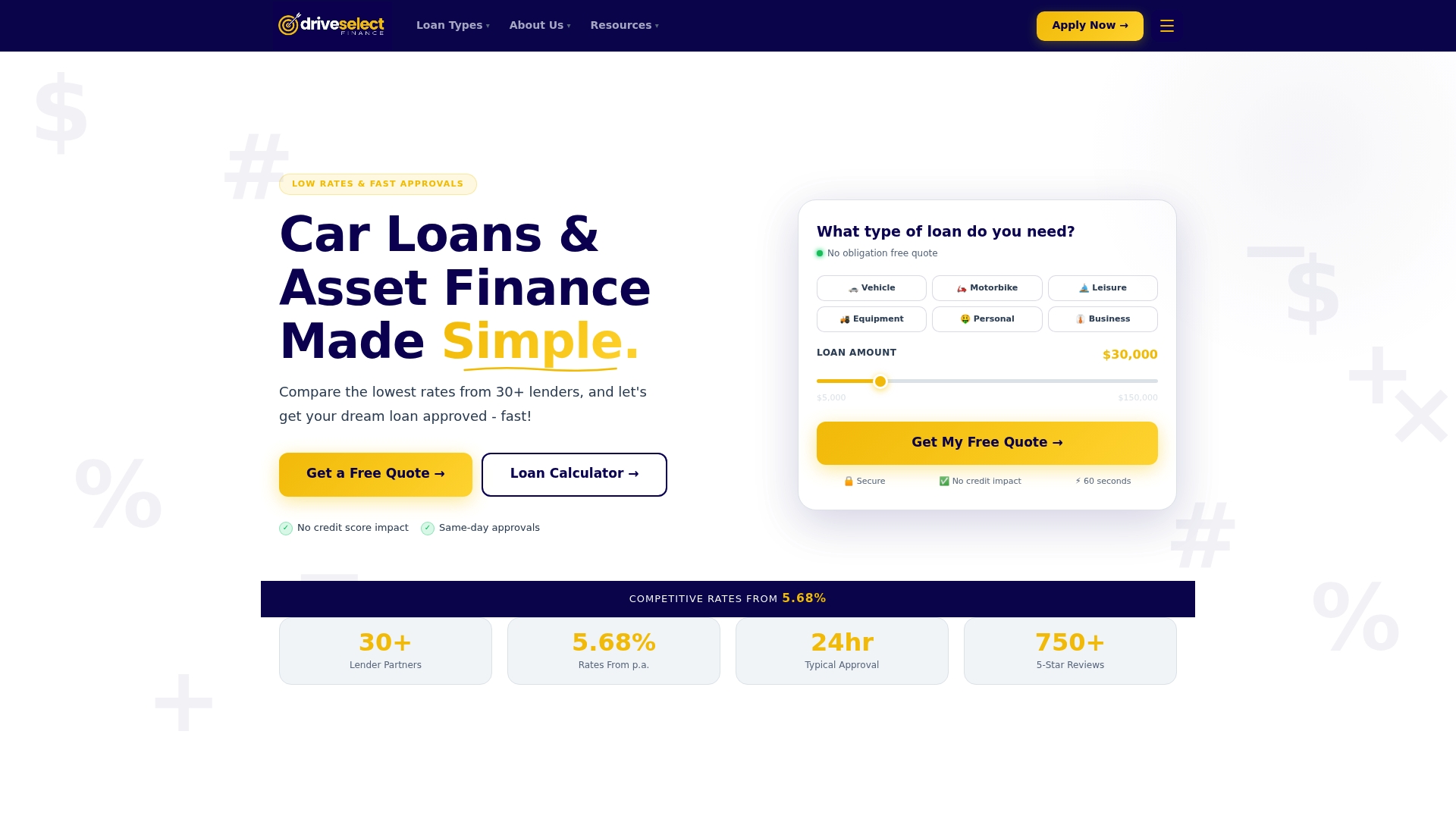

Driveselectfinance can match your budget to the right loan

Building a realistic car budget is the first step. Finding a loan that fits it is the second. Driveselectfinance works with a panel of 30+ trusted lenders to compare rates and match you with financing that suits your actual budget, not just your maximum borrowing capacity.

Whether you are buying new or used, Driveselectfinance structures car loans around your full ownership costs, not just the purchase price. Getting pre-approved through Driveselectfinance takes the guesswork out of dealership negotiations and gives you a clear spending limit before you walk onto the lot. Flexible loan terms, competitive rates, and access to multiple lenders mean you compare real options rather than accepting the first offer you receive.

FAQ

What is the average cost of owning a car in Australia?

The average annual ownership cost is approximately $11,577, or $965 per month, including fuel, insurance, maintenance, and depreciation.

How much should I budget beyond the car's purchase price?

Budget at least $2,000 to $3,000 for on-road costs upfront, plus approximately $5,000 per year for ongoing running costs including fuel, servicing, and insurance.

Does registration cost the same in every Australian state?

No. Registration and CTP fees vary significantly by state. South Australia charges around $430 annually while the ACT can exceed $1,200 for the same vehicle class.

Is it cheaper to buy a new or used car in Australia?

Used cars cost less upfront and avoid the 20–25% first-year depreciation hit that new vehicles carry. Certified pre-owned vehicles offer the best balance of lower cost and warranty protection.

What is the biggest mistake buyers make when budgeting for a car?

The most common mistake is borrowing to the maximum loan limit without accounting for running costs, which can add $750 to $900 per month on top of the loan repayment.